When a broker COO compares two liquidity providers, the first metric on the page is almost always quoted spread on EUR/USD. It is the wrong metric, and it has been the wrong metric for at least a decade — but it persists because it is easy to compute and easy to put in a sales deck.

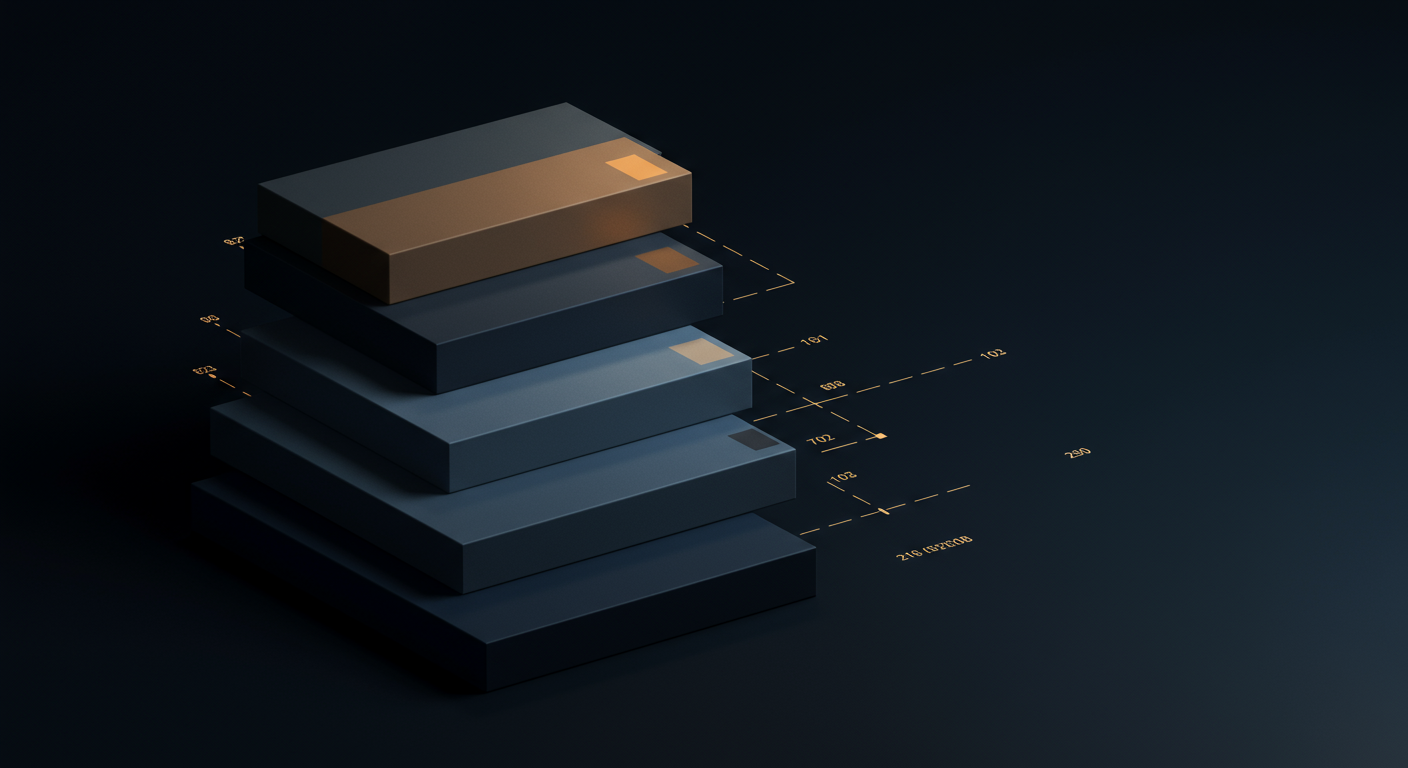

The actual cost of wholesale liquidity is a stack of seven components. Quoted spread is one of them. The others, properly quantified, can swing the all-in cost of execution by more than the spread itself.

Component 1 — Quoted spread

The simplest piece. Top-of-book bid-ask, time-weighted across your trading sessions. This is the only component that appears on the quote screen, and it accounts for roughly 30–50% of all-in cost for a mid-sized broker.

Component 2 — Effective spread

Effective spread is the difference between the price you actually got and the mid at the moment of order arrival. It can be wider or tighter than the quoted spread depending on aggression, latency, and venue behaviour. Our microstructure survey article goes into the measurement in detail.

Component 3 — Last-look slippage

On any venue that uses last-look, some orders are rejected and re-quoted at a worse price. If the rejection policy is symmetric, this is a wash in expectation. If it is asymmetric — and many venues still are — it costs the consumer 0.3 to 0.8 pips per million on average. This is the single largest hidden cost in 2026, and the one buyers most often fail to measure.

Component 4 — Capacity decay

The second slice of a large order is rarely filled at the same price as the first. The decay curve depends on the depth profile of the venue and the smartness of the smart router. On thin venues, a USD 20m EUR/USD clip can pay 0.8 pips more on the second half than the first.

Component 5 — Per-million commission

The explicit fee, billed by the provider. Usually USD 5–25 per million in FX, more in CFDs. This is transparent and the easiest component to negotiate; treat it as a known constant rather than a focus of optimisation.

Component 6 — Credit cost

If you are running pre-funded margin, the cost is the opportunity cost of the working capital sitting at your provider's bank. If you are running on a credit line, the cost is the all-in line fee plus any covenant burden. For a mid-sized broker this can be a five-to-seven-figure annual line item.

Component 7 — Operational and connectivity cost

FIX engines, drop-copy, reconciliation, monthly platform fees, the headcount required to run the relationship. Often invisible because it is split across infrastructure and ops budgets, but for a small broker it can dominate per-million economics.

Putting it together — the all-in number

Sum all seven components, normalise to pips per million traded, and that is your all-in cost. In a typical 2026 mid-sized FX broker book, the breakdown looks roughly like this:

- Quoted spread: 0.4 pips

- Effective vs quoted gap: 0.2 pips

- Last-look slippage (asymmetric venue): 0.5 pips

- Capacity decay on large clips: 0.3 pips

- Commission (USD 8 / m): 0.08 pips

- Credit cost (annualised): 0.05 pips

- Ops and connectivity: 0.05 pips

All-in: ~1.6 pips per million — of which the headline `spread' was only a quarter.

How Drovix prices each component

Drovix's commercial model is structured so that components 5 through 7 are explicit line items on every monthly statement. Components 1 through 4 are reported in the monthly execution-quality pack at venue-tag granularity, which means you can see exactly where your money is going.

We default to symmetric last-look venues and route around asymmetric ones automatically. We publish capacity curves per instrument so you can size clips against real depth rather than the top-of-book illusion. None of this is novel — it is what serious institutional plumbing should look like — but it is surprisingly rare in the prime-of-prime layer.

What to do tomorrow morning

Ask your incumbent provider for the seven-component breakdown on your own flow for the last quarter. If they cannot produce it, that is a finding. If they can produce it but it shows a different shape than this article, that is information about your flow. Either way, you will know more than your competitors who are still comparing quoted spreads on a screen.

Analyst Desk

Drovix Research Desk

Institutional Research

Drovix Research Desk publishes institutional-grade analysis covering macro events, cross-asset correlations, and execution insights for professional market participants.